Unlocking Global Access to GLP-1 AOMs Requires Moving Beyond Disease Recognition to Demonstrating Broader Value

Summary

To enable global access to GLP-1 AOMs, manufacturers must demonstrate multidimensional value along the full care continuum and across the range of obesity linked-indications.Background

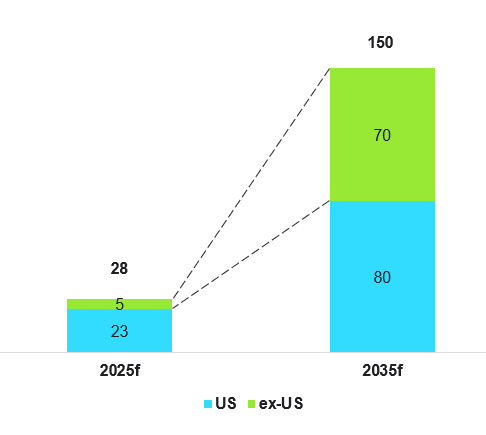

Over the coming years, the market for anti-obesity medicines (AOMs), including glucagon-like peptide-1 (GLP-1) receptor agonists, is projected to grow more rapidly in ex-US markets than in the US. Forecasts position the global AOM market as a $150 billion opportunity within the next decade, with contributions split nearly equally between ex-US ($70 billion) and US ($80 billion) markets (Figure 1).

Figure 1: Forecasted US and Ex-US AOM Market Size (2025–2035), US$ Billions

Data adapted from multiple industry estimates.

Originally developed for diabetes, GLP-1s are now riding a dual-growth trajectory – sales are expected to be driven equally by applications in diabetes and obesity by 2030. While GLP-1s are typically reimbursed in diabetes, obesity prescriptions are mostly self-funded, creating an access divide that limits uptake to those who can afford to pay. Reimbursement remains a key challenge: a market leader in GLP-1 AOMs reported that in 2024, 80% of their ex-US AOM sales were out of pocket, a trend consistent with 2022.

The lack of reimbursement creates an inverse access dynamic that limits care for socioeconomically disadvantaged populations in which obesity is more prevalent. If GLP-1 AOMs are to fulfill their potential, not just commercially but in reshaping health outcomes, reimbursement globally must evolve and expand.

Treating the Risk, Not the Weight

As of 2024, around 15 markets provided restricted reimbursement for liraglutide to treat obesity, and even fewer markets reimbursed semaglutide AOMs. Whether countries recognize obesity as a medical condition does not dictate AOM reimbursement decisions. For example, Germany and Italy recognize obesity as a medical condition but do not reimburse GLP-1 AOMs, classifying them as a lifestyle or non-essential drug, respectively. Conversely, while England has yet to recognize obesity as a medical condition, semaglutide, liraglutide and tirzepatide AOMs are reimbursed for eligible individuals.

This paradox exposes a deeper truth: public payers do not reimburse treatments merely for weight loss, as obesity in itself is not believed to impose costs on the healthcare system. Rather, it is the obesity-related diseases that are recognized as the primary sources of clinical and economic burden. As such, beyond just weight reduction, demonstrating how GLP-1 AOMs can reduce the incidence or severity of related diseases is key to achieving favorable reimbursement decisions. For example, in France’s reimbursement assessment of semaglutide AOM, its clinical value in reducing the risk of cardiovascular events such as myocardial infarction and stroke was considered. Similarly in England, the cost-effectiveness model developed for liraglutide AOM, which was later also adapted for semaglutide AOM, incorporated its potential to lower the long-term risk of myocardial infarction, angina, and stroke. Germany, on the other hand, declined to reimburse semaglutide AOMs even for severe obesity, although it indicated potential consideration for its use in reducing cardiovascular event risk in patients with a history of cardiovascular disease (CVD).

This landscape highlights a clear imperative for manufacturers: reimbursement depends on demonstrating meaningful benefits in managing or preventing high-burden, obesity-related diseases. In response to public payer priorities and expectations of GLP-1 AOMs, manufacturers must adapt and sharpen their strategies to position GLP-1 AOMs not just as treatments, but as transformative investments that pivot healthcare from reactive spending toward proactive risk mitigation that unlocks systemic cost savings.

Emphasize Cost Savings and Broaden Clinical Applicability

To support favorable reimbursement decisions in the immediate to near-term, manufacturers must provide compelling evidence showing that GLP-1 AOMs are a cost-effective way to lower the risk of related diseases. For example, a manufacturer-funded study focusing on individuals over 45 years old with established CVD (a subpopulation that composes 10% of the total population with obesity), found that semaglutide AOM was considered to be twice as cost-effective as treating the broader obese adult population. This spotlights a tension in access strategy: targeting high-risk subgroups where the clinical and cost impact is more pronounced increases reimbursement success but caps the wider opportunity for GLP-1 AOMs.

To offset the limitations of a narrower eligible population, manufacturers will need to broaden the clinical reach of GLP-1 AOMs by demonstrating obesity’s role as a risk factor across a wider range of related diseases. Trials are already exploring the benefits of GLP-1 AOMs beyond CVD, such as liver cirrhosis, knee osteoarthritis, and chronic kidney disease. Demonstrating clinical benefit across a wider spectrum of diseases enhances the perceived value and utility of GLP-1 AOMs, and broadens its eligible patient population, facilitating improved outcomes for more individuals.

Portfolio Differentiation for End-to-End Care

Although GLP-1 AOMs are currently indicated for individuals who meet the Body Mass Index (BMI) threshold for obesity and have existing obesity-related comorbidities, the reality is that health risk exists on a continuum and not a binary state. Effective management of obesity and related diseases should start well before an individual’s BMI crosses a certain threshold or comorbidities develop, and it must continue even after individuals return to a healthier state to support secondary disease prevention and long-term health maintenance.

In the long-term, manufacturers that treat GLP-1 AOMs as episodic care will lose market share to those who treat them as the anchor to an obesity ecosystem. The opportunity lies in building a differentiated portfolio of solutions that span the full spectrum of the patient journey – from at risk stages to diagnosis, treatment, secondary prevention and long-term management. For example, therapeutically modified GLP-1 AOMs developed for individuals who are at risk of obesity-related diseases but do not yet qualify for standard GLP-1 AOMs could provide earlier and safer risk management options that alter the course of disease.

The Role of Manufacturers in the New Era

Pharmacotherapy alone will not solve today’s obesity crisis. Effective obesity management solutions must extend beyond pharmacological treatments to offer a more holistic approach to disease prevention. In the Australian Pharmaceutical Benefit Advisory Committee’s review of semaglutide AOM, which was ultimately not recommended for reimbursement, reviewers acknowledged that pharmacotherapy is just one aspect of the public health response to obesity.

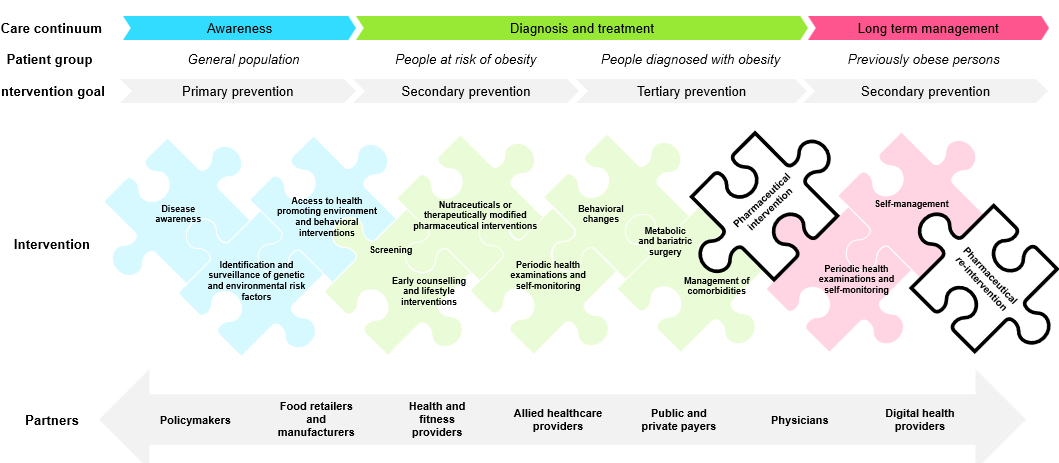

By offering tailored solutions at each stage of the patient journey, manufacturers can create value for a broader range of individuals across the obesity continuum and establish themselves as an end-to-end partner in disease prevention and health management (Figure 2). Leading manufacturers are already partnering with digital health providers to offer lifestyle interventions such as diet planning support and explore innovations like body composition scanning through mobile apps.

The push for holistic, integrated care is not unique to obesity. It mirrors trends across other therapeutic areas where innovators have moved beyond the pill to offer patient-centric solutions in disease tracking, behavior change, digital therapeutics, and more. It is only a matter of time before this approach becomes embedded in obesity care, and manufacturers must stay ahead of the curve in offering holistic, continuous, and personalized care (Figure 2).

Figure 2: Pharmaceutical Intervention is Just One Piece of the Obesity Care Continuum

The GLP-1 AOM market is rapidly expanding, and reimbursement can unlock significant untapped opportunities beyond self-pay segments. To meet public payers’ expectations, manufacturers must evolve beyond their traditional role as drugmakers to be true care partners across the care continuum. This means delivering value through integrated healthcare solutions that support individuals at every stage of care, rather than focusing solely on reactive treatments.

The GLP-1 AOM market is rapidly expanding, and reimbursement can unlock significant untapped opportunities beyond self-pay segments. To meet public payers’ expectations, manufacturers must evolve beyond their traditional role as drugmakers to be true care partners across the care continuum. This means delivering value through integrated healthcare solutions that support individuals at every stage of care, rather than focusing solely on reactive treatments.

Dive Deeper

With deep expertise in market access, value communication and strategic evidence generation, Avalere Health is well-positioned to help manufacturers navigate evolving payer expectations to enable value-driven engagement and become true partners in the healthcare ecosystem.

This Insight is the fourth in a series on GLP-1s that explored compounding, evidence for expanding on- and off-label uses, and coverage limitations. To dive deeper on any of these topics or learn how you can tap into Avalere Health’s expertise on GLP-1s and AOMs, connect with us.

Services

produces measurable results. Let's work together.