The New Stakeholder Economics of Part D After the IRA

Summary

The implementation of the IRA’s Part D redesign and Medicare drug price negotiation in 2026 will have varying impacts across plan types and therapeutic areas.On January 1, 2025, the Inflation Reduction Act (IRA)’s Medicare Part D redesign provisions went into effect for all Part D drugs. These provisions lower the beneficiary out-of-pocket (OOP) cap and increase plan and manufacturer liability, particularly in the catastrophic phase of coverage. Additionally, starting in 2026, select drugs will also be subject to Medicare drug price negotiation, further impacting market dynamics.

Avalere Health examined the separate and combined effects of Part D redesign and Medicare negotiation on plan, manufacturer, and beneficiary financial liability.

Impact of Part D Redesign Across Stakeholders

Plans: The effects of Part D redesign on plans depend on plan type, therapeutic area (TA), low-income subsidy (LIS) vs. non-LIS patient mix, and a product’s eligibility for specified or specified small manufacturer phase-in.

- Plan Type: Across analyses, standalone Prescription Drug Plans (PDPs) with higher enrollment among dual-eligible or LIS beneficiaries were more likely to have increased financial liability under Part D redesign compared to Medicare Advantage Prescription Drug Plans (MA-PDs) and plans with greater shares of non-LIS enrollees.

- Therapeutic Area: Estimated increases in plan liability were typically greatest for TAs where spending is primarily concentrated in the catastrophic phase. However, projected increases can be different even within TAs (e.g., between different cancer types). Across various TAs—including cardiovascular disease, oncology, and autoimmune conditions—net plan liability changes pre- vs. post-IRA could vary substantially for different competitor products within the same class depending on product pricing and patient mix, even when assuming identical rebate levels.

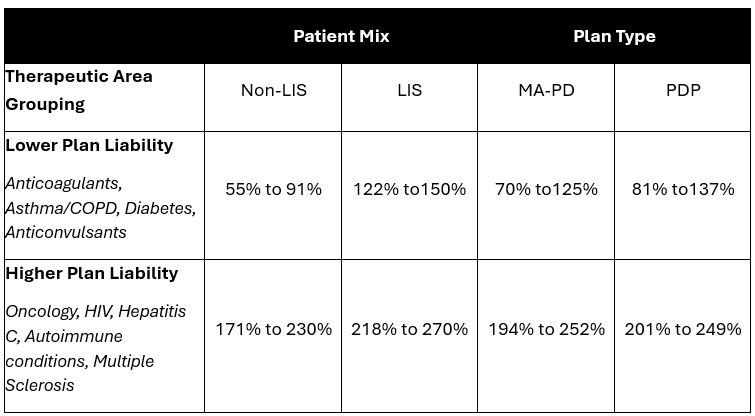

- Patient Mix: For non-LIS beneficiaries, projected net plan liability following Part D benefit redesign was estimated to increase between 55% to 91% for non-LIS beneficiaries with common chronic disease conditions such as anticonvulsants, diabetes, asthma/COPD, anticoagulants, and antipsychotics. This compares to a 171% to 230% increase in pre-vs. post-redesign net plan liability for specialty TAs such as oncology, HIV, autoimmune, multiple sclerosis, and Hepatitis C (Table 1). These changes in liability were even greater for LIS beneficiaries and for PDPs vs. MA-PDs.

- Specified Manufacturer or Specified Small Manufacturer Phase-In Eligibility: Changes in plan liability after Part D redesign also depend on whether a manufacturer is eligible for the specified or specified small manufacturer phase-in. The phase-in gradually increases mandatory discount liability for qualifying manufacturers over several years while temporarily increasing plan liability during this transition period. For example, Avalere Health’s analysis of drugs for pain management and hormone treatments that qualify for the specified manufacturer discount found that increases in plan liability for these products for LIS beneficiaries would range from just over 100% to almost 600% pre- vs. post- Part D benefit redesign.

Table 1: Change in Plan Liability by Therapeutic Area Grouping, LIS Status, and Plan Type

Manufacturers: Under Part D redesign, manufacturer liability changed with the removal of the coverage gap and the implementation of new mandatory discount liability in both the initial coverage period and catastrophic phase. As such, changes in manufacturer liability pre- vs. post-Part D redesign vary depending on where the drug falls within the benefit structure based on product pricing, beneficiary medication utilization, patient mix (LIS vs. non-LIS), and eligibility for the discount phase-ins. Avalere Health’s analyses found that while some products may see a decrease in mandatory manufacturer discounts compared to pre-IRA, other products will have increases in discount liability of over 500% for certain specialty drugs.

Plans and Manufacturers: As a result of changes to manufacturer and plan liability under Part D redesign, both stakeholders will need to reevaluate their contracting and pricing approaches. An Avalere Health analysis found that for some products, higher list price increases will raise manufacturer discount liability. For many products, particularly those in competitive classes where plan liability has increased most under Part D redesign, manufacturers may need to increase rebates to Part D plans to maintain preferred formulary positioning.

Beneficiaries: Starting in 2025, annual beneficiary OOP costs will be capped at $2,000.

- Plan Type and Formulary: Reductions in OOP spending may be greater for those enrolled in enhanced Part D plans due to a change implemented by the Centers for Medicare and Medicaid Services (CMS) to count the value of enhanced plan benefits towards patient progression towards the OOP cap. However, beneficiary OOP costs are also driven by changes to Part D formularies, including tier placement and shifts from copays to coinsurance. For many beneficiaries with spending below the cap, these changes may increase overall OOP costs in 2025.

- Therapeutic Area: The impact of this provision will vary across TAs: beneficiaries taking specialty medications are more likely to see the greatest reductions in OOP costs due to the cap. For example, some TAs like multiple sclerosis are projected to have larger beneficiary OOP cost reductions than other TAs like mental health.

CMS: With higher plan liability and reduced government reinsurance in the catastrophic phase, federal spending under Part D redesign is estimated to shift from reinsurance to direct subsidy payments. However, the extent of the reduction in federal reinsurance costs pre- vs. post-benefit redesign are estimated to vary by product, depending on where spending for the drug falls within the Part D benefit (e.g., specialty products with spending primarily in the catastrophic phase vs. products for chronic conditions with spending primarily below the catastrophic threshold).

Combined Impact of Part D Redesign and Medicare Drug Price Negotiation

The first Maximum Fair Prices (MFPs) for selected drugs will come into effect in 2026, which many expect to further shift market dynamics.

Interactions with Part D Redesign: According to Avalere Health’s analysis on the combined impacts of Part D redesign and Medicare negotiation, MFPs negotiated at 75% of ceiling price (assuming no discretionary rebates) would increase net plan costs for nine out of the 10 Initial Price Applicability Year 2026 drugs compared to pre-IRA costs. Under this scenario, net plan costs could increase from about 40% to over 2,000%. A separate analysis showed similar results across different product archetypes: specialty drugs with low rebates, highly rebated chronic disease drugs, and highly rebated specialty biologics. The analysis found that MFPs may not completely offset increased plan liability from the Part D benefit design changes.

- Negotiation-Only Effects: When isolating the effects of Medicare negotiation in 2025 to 2026, MFPs negotiated at 75% of the ceiling price have mixed impacts on plan liability and premiums, with plan liability increasing for some products while decreasing most for products that currently have lower rebates. A similar analysis for respiratory products found that MFPs negotiated at 70% of the ceiling price also have mixed impacts on plan liability, with some products having similar liability before and after Medicare negotiation for other products lowered net plan costs more substantially.

- New Contracting Strategies: Manufacturers of selected drugs and their competitors may need to reevaluate contracting strategies, particularly for products subject to an MFP that results in significant loss of rebates for plans relative to non-selected competitors Several analyses found that plan liability for different TAs, including products treating cardiovascular conditions, oncology products, and autoimmune diseases, depends on the pricing and rebating strategies of both the selected vs. non-selected competitor drugs. In some scenarios, a non-selected drug offering rebates could result in lower estimated net plan liability compared to a selected drug with an MFP . However, the level of additional rebating needed to achieve lower net plan liability for a non-selected drug was dependent on rebate levels in the therapeutic area pre-IRA. Another Avalere Health analysis found that even if two competitor products are negotiated in future years at the same MFP, they may result in different plan net liability changes due to variations in patient mix and utilization

Next Steps

As the January 2026 implementation of Medicare drug price negotiation approaches, manufacturers and plans should assess how interactions with Part D redesign will drive market shifts and shape strategic priorities. Avalere Health has access to data that allow for near-real time analysis of changes in 2025, including impacts on beneficiary utilization via a data use agreement with the CMS Virtual Data Research Center, and can serve as a partner to help navigate and evaluate the evolving Part D and COVID landscape. Connect with us here.

Methodology:

The analyses referenced in this publication use CMS’s 2020-2024 Medicare Part D drug event (PDE) data to simulate the impact of Part D redesign and Medicare drug price negotiation pre-IRA (2023) and post-IRA (2025+). 100% Medicare PDE data for several analyses outlined here that utilized 2020-2021 claims was accessed by Avalere Health via a research collaboration with Inovalon, Inc. by a research focused CMS Data Use Agreement. A few analyses used 2022–2024 100% Medicare PDE data through an agreement with CMS, wherein Avalere Health has access to CMS’s Chronic Condition Warehouse Virtual Research Data Center. Note that analyses referenced did not incorporate CMS’s change to include plan enhancements towards true out-of-pocket costs for beneficiaries.

Services

produces measurable results. Let's work together.