Buy and Bill Provides Key Revenue for Physician Practices

Summary

The acquisition and administration of Part B drugs provides key revenue for many physicians, with high uptake in some specialties.Background

Medicare beneficiaries can obtain prescription medication through both Part B and Part D. While standalone Part D plans cover most outpatient drugs (e.g., self-administered pills that patients pick up at a pharmacy), Part B covers physician-administered drugs as part of the medical benefit. Physician-administered drugs are often administered in an office or other clinical setting, such as an ambulatory infusion center, but may also be given in the home. Common examples of Part B drugs include chemotherapies and other cancer treatments or infusions used by rheumatologists, gastroenterologists, and immunologists to treat autoimmune diseases.

Under Medicare Part B, physician-administered drugs are reimbursed at average sales price (ASP)+6%, or at the average sales price of the drug with an add-on payment equivalent to 6% of that drug’s average sales price (4.3% after the application of statutory sequestration requirements). To collect the data needed to calculate the ASP-based Medicare payment amount for each Part B drug code, CMS requires certain manufacturers to submit quarterly ASPs and the sales volume for each of their National Drug Codes (NDCs). Manufacturers calculate a quarterly ASP for each NDC by dividing total sales by the sales volume. Manufacturers must also report to CMS certain product information for each NDC, including product strength as well as information that CMS uses to determine the package size and package quantity—each of which affects the calculation of the Medicare payment amount.

Under this methodology, physician practices are reimbursed under a “buy and bill” system, whereby the physician practice purchases the drug from a manufacturer, wholesaler, or distributor and keeps it in inventory until administration to a patient. Physician practices then submit a claim to secure reimbursement for the administration of the drug as well as reimbursement for the drug itself under the ASP+6% methodology.

Analysis

Because of the prevalence and importance of buy and bill as a reimbursement methodology across many therapeutic areas, Avalere Health sought to understand Part B reimbursement dynamics for physician practices in several specialties. Factors contributing to variance in buy and bill revenue across physician practices may include the number of drug products in a specialty that require physician administration, as well as a practice’s ability to finance high-cost specialty drug inventory.

Avalere Health used 100% Medicare fee-for-service data to access J code claims and payment data for 2018 through 2023. The analysis was limited to claims with Medicare as the primary payer where J codes (drug codes) appear. Avalere Health used the provider specialty referenced on the claim to associate claims with four specialties: allergy/immunology, gastroenterology, neurology, and rheumatology. Providers were then aligned to a practice based on the tax identification number referenced on Part B claims.

Analysis of the 100% Medicare claims data allowed Avalere Health to determine each specialty practice’s buy and bill J code payments as a percentage of its total payments to explore differences between each specialty’s relative reliance upon buy and bill as a revenue source.

Results and Discussion

Across physician practices in the four specialties analyzed, Avalere Health found that the proportion of total revenue attributable to J codes via buy and bill increased from 2018 to 2023. Figure 1 shows that, by 2023, the average percentage of total revenue attributable to buy and bill ranged from 15% in neurology practices to 56% in rheumatology practices. In 2023, the interquartile range (IQR) – representing the middle 50% of the distribution – ranged from 13% in neurology practices to 65% in allergy/immunology practices.

Figure 1. Practice J Code Revenue as a Share of Total Revenue, by Specialty, 2018 vs. 2023

Note: These results represent the full distribution of practices billing in each specialty, with practices of all sizes (i.e., single physicians to practices with more than 100 physicians) represented.

The range of these results suggests varying levels of uptake with respect to buy and bill across practices in key specialties. Physician practices in some specialties, such as rheumatology, appear to rely substantially upon buy and bill revenue as a share of total revenue, while those in other specialties, such as neurology, do not. Furthermore, wide IQRs suggest greater variability in revenue structure for specialties like allergy/immunology. These variations could be attributable to differences in service mix, the availability and approved indications of Part B drugs, physician employment and practice dynamics, geographic and demographic nuances, and other factors that affect physician behavior.

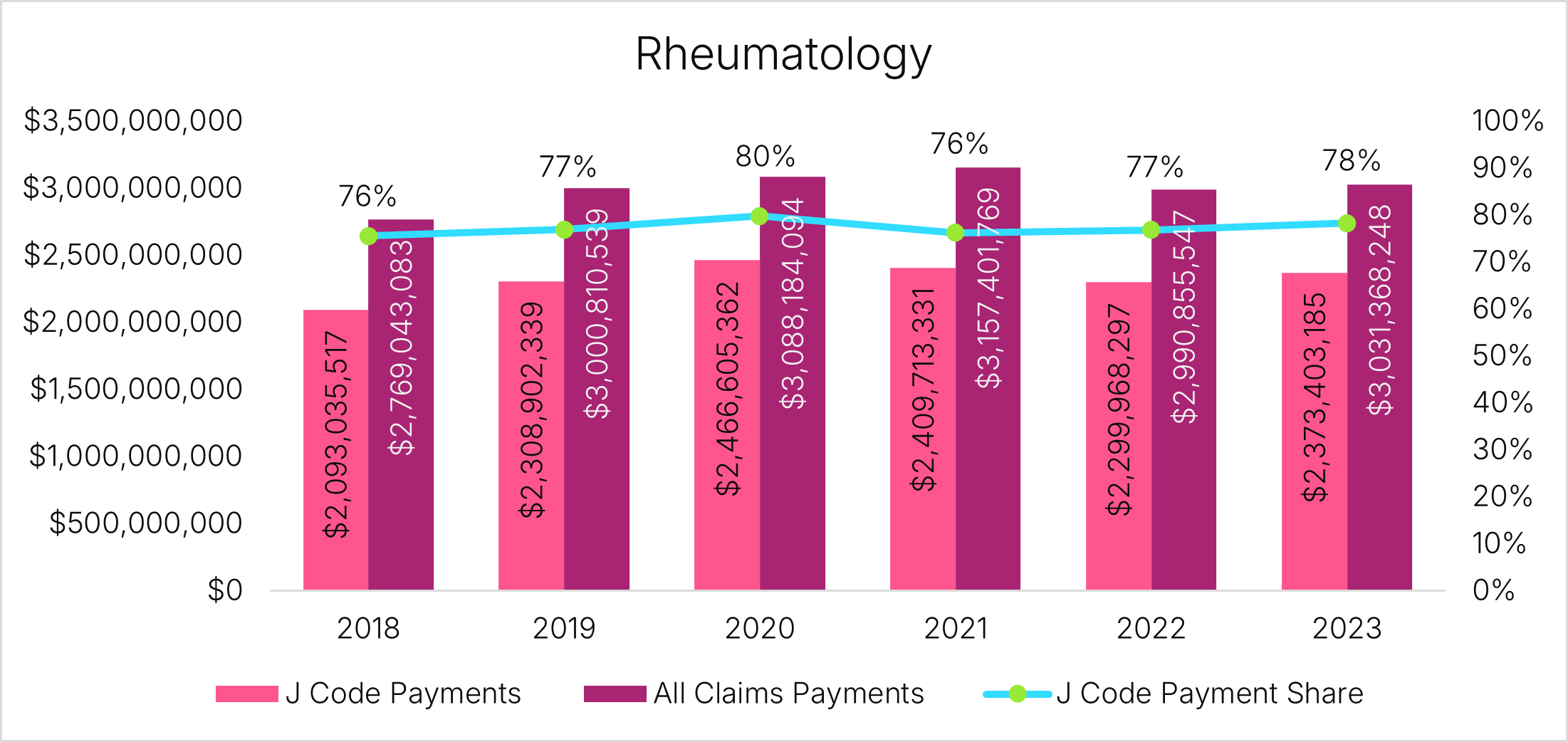

At the specialty level, Avalere Health’s analysis reveals differences in the growth of buy and bill revenue over time. Figures 2 and 3 offer a comparison of rheumatology, a relatively mature specialty with respect to buy and bill, and neurology, a specialty where buy and bill has seen less penetration.

Figure 2. Total Medicare Payments, J Code Payments, and J Code Payments as a Percentage of Total Medicare Payments, Rheumatology, 2018-2023

Figure 3. Total Medicare Payments, J Code Payments, and J Code Payments as a Percentage of Total Medicare Payments, Neurology, 2018-2023

Figure 3. Total Medicare Payments, J Code Payments, and J Code Payments as a Percentage of Total Medicare Payments, Neurology, 2018-2023

These trends offer insights into the service mix and practice structures of different specialties. In rheumatology, the percentage of total Medicare payments attributable to J codes remained between 75% and 80% from 2018 through 2023. This stability reflects an enduring reliance on buy and bill revenue in the specialty, as well as potentially limited opportunity for further uptake. In contrast, the substantial growth of buy and bill in neurology – which increased as a percentage of total revenue from 13% in 2018 to 22% in 2023 – reflects new and evolving opportunities for those specialists to infuse drugs. For example, infusions are increasingly used to treat multiple sclerosis and myasthenia gravis, and new drugs to treat Alzheimer’s disease are expected to further increase neurology infusion volume and revenue.

Looking Ahead

The uptake and profitability of buy and bill for Part B drugs remains an important consideration in the current US healthcare landscape. As physician practices pursue strategies to maintain or expand service offerings and to remain financially viable, the acquisition and administration of specialty drugs can prove a meaningful source of practice revenue. At the same time, continued scrutiny on drug pricing and supply chains – especially in the context of the Inflation Reduction Act – make attention to buy and bill crucial for stakeholders involved in specialties with meaningful Part B drug revenue exposure.

To learn more about Part B, buy and bill, or other drug trends, connect with us.

Services

produces measurable results. Let's work together.