2027 Medicare Advantage Payments: Market Implications

Summary

MA payment growth slows in 2027, possibly signaling further disruption in plan availability and enrollment.On April 6, the Centers for Medicare & Medicaid Services (CMS) released the Calendar Year (CY) 2027 Medicare Advantage (MA) and Part D Rate Announcement and the MA Ratebook. Together, these documents set the foundation for MA plan payments in 2027 and provide insight into the financial environment plans will face as they make MA and Part D plan benefit decisions in the coming months.

The Rate Announcement details national MA and Part D payment policies (including MA payment trends and updates to risk adjustment) while the MA Ratebook contains the county-level benchmark rates. The county level benchmark rates effectively represent the maximum amount that CMS will pay an MA plan to provide coverage to a beneficiary of average health status in a given county; even modest changes to these rates can have meaningful implications for plan participation and market stability.

2027 MA Payment Changes

For 2027, CMS expects national plan revenue to increase by 2.48% relative to 2026. This increase is driven by an effective growth rate of 5.33%, offset by a 2.65% decrease due to changes in risk adjustment. While CMS expects the 2.48% increase to provide an additional $13 billion to MA plans in 2027, this increase is less than half of the 5.06% increase provided in 2026. Given that the MA market experienced notable disruption in plan year 2026, the more modest increase in MA plan payments in 2027 could result in additional market disruption.

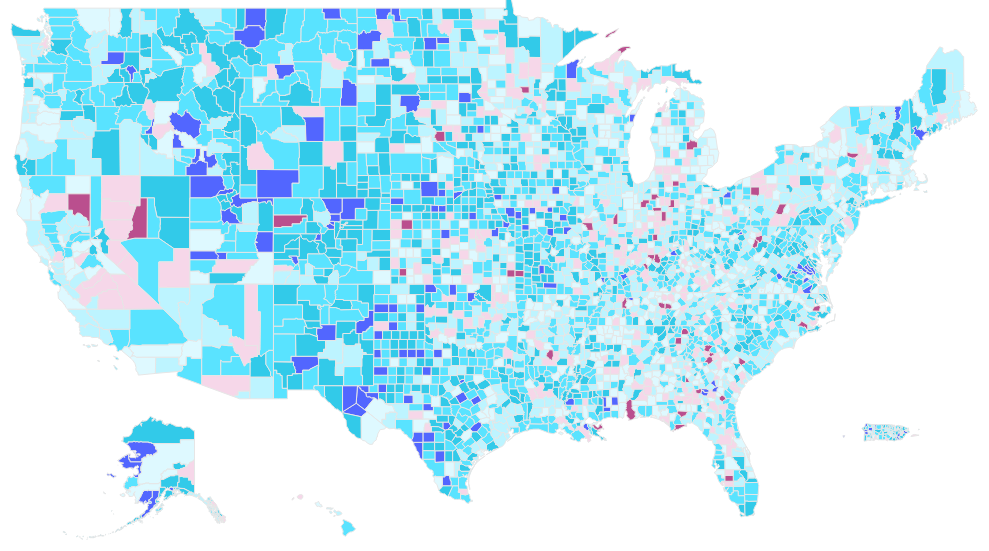

The effective growth rate and changes to risk adjustment are reflected in the county-level benchmark rates (see Figure 1). In 2027, the county level benchmarks range from a low of $685.99 per beneficiary per month in Santa Isabel County, Puerto Rico to a high of $2,735.00 in North Slope County, Alaska. The year-over-year percentage changes within counties ranged from a decrease of 4.5% to an increase of 19.8%.

Figure 1: Percentage Change in MA Benchmark by County, 2026−2027

Market Impacts of MA Rate Changes

MA plans must finalize their 2027 plan offerings by June 1, 2026, including decisions about geographic participation, benefit design, and enrollee premiums. These decisions may be influenced by the 2.48% increase in plan revenue.

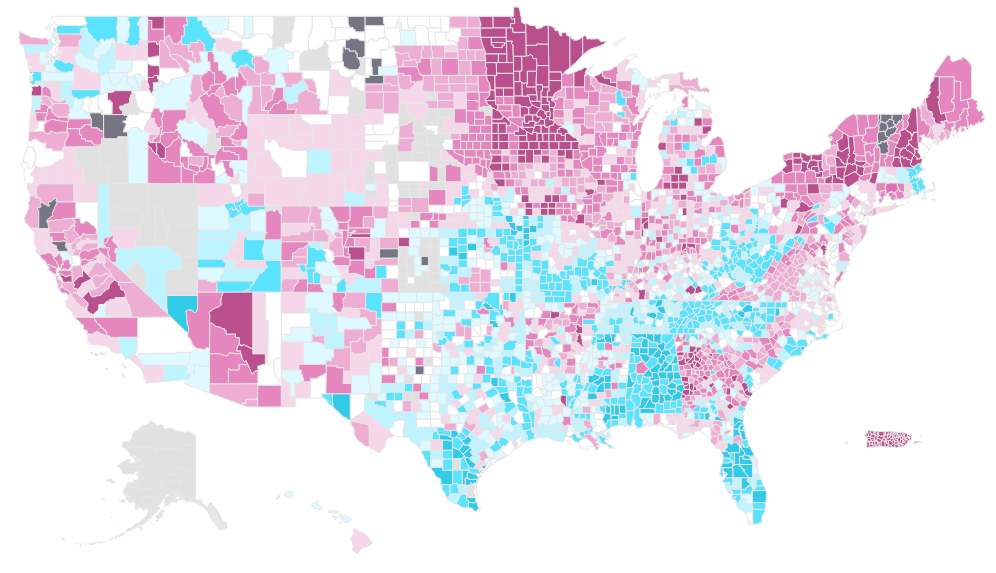

The change in plan offerings and enrollment from 2025 to 2026 provides important context as stakeholders assess potential market impacts of the 2027 MA payment rates. Despite an expected plan payment increase of more than 5% in 2026, a significant number of beneficiaries were impacted by plan terminations. As shown in Figure 2, nearly 50% of counties saw the termination of at least one MA plan, and in 21 counties all MA plans were terminated for 2026. Rising medical costs, increased drug utilization, and uncertainty in future costs may have driven plan terminations in 2026.

Figure 2: Change in the Number of MA Plans Offered by County, 2025− 2026

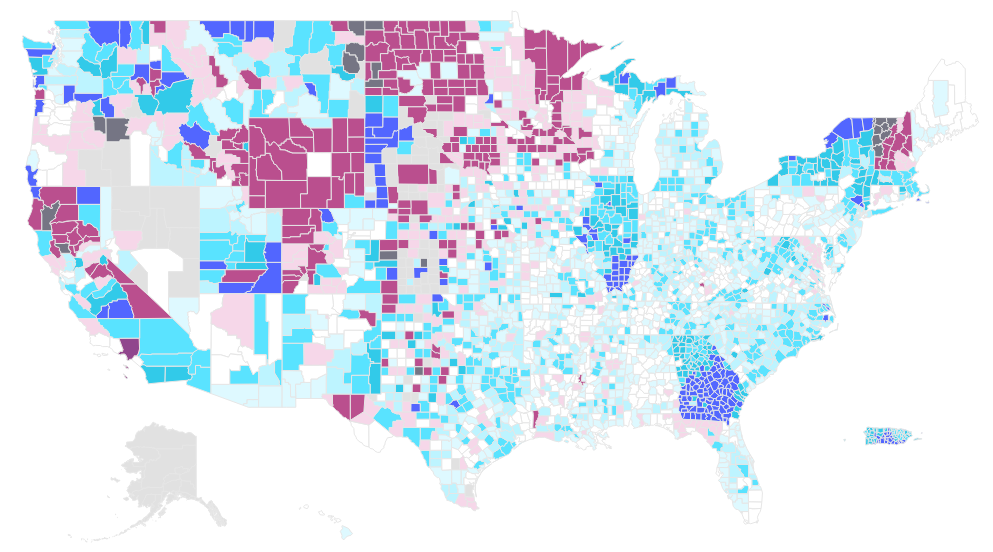

Plan terminations directly impact beneficiary access to MA coverage. As illustrated in Figure 3, many of the counties that experienced plan terminations saw declines in MA enrollment from 2025 to 2026.

Figure 3: Change in Enrollment by County, 2025−2026

Stakeholder Considerations

Plans: Given the more modest MA payment growth in 2027, plans should evaluate cost pressures, operational efficiency, provider relationships, market competition, and quality performance. Limited payment rate growth heightens the importance of strong Star Ratings to maximize plan revenue. Given that enrollment may shift between plans in the MA market, plans should also monitor competitor actions to better anticipate future enrollment and cost trends. These considerations can inform decisions on geographic participation, premiums and cost sharing, supplemental benefits, formulary coverage, and utilization management strategies.

Beneficiaries: As MA plans respond to 2027 payment changes, beneficiaries may face changes in plan availability, benefit design, premiums, drug coverage, and access to supplemental benefits. These changes are likely to vary by MA organization (MAO) and geography and could result in uneven impacts across markets. As plan offerings shift, beneficiary access to medical care and prescription drugs may be affected. The evolving MA landscape underscores the importance of ensuring beneficiaries have clear, accessible information to make informed coverage decisions.

Providers: Providers should be aware of how CMS funding can impact plan financials, offerings, and benefits. Plans may seek to renegotiate the rates they pay to providers to manage their costs. Additionally, Providers who are currently paid based on a percentage of plan revenue could experience costs that increase at a rate that exceeds the overall 2.48% increase in MA payments . If plans are terminated or benefits are reduced, some beneficiaries may seek new coverage options, either through a different MA plan or through traditional Medicare. Providers should understand their contracting across MAOs and how their revenue will change in the event that there is significant market disruption in the geographies in which they provide care.

Supplemental Benefit Vendors: As plans weigh their costs and benefit design for the 2027 plan year, coverage of certain supplemental benefits could be discontinued. Given the limited increase in plan revenue, it is especially important for vendors to have evidence demonstrating the value of their supplemental benefits.

Manufacturers: In the 2027 plan year, beneficiaries may experience changes in plan availability, premiums, drug coverage, and out-of-pocket costs, which can directly affect access to both physician-administered and prescription drugs. Beneficiary experiences can vary significantly across geographies and MAOs, and even within a single MAO.

Further, access to drugs can differ depending on MA plan type. For example, certain special needs plans that enroll beneficiaries that are dually eligible for Medicare and Medicaid are more likely to provide prescription drug coverage under the Part D defined standard benefit rather than an enhanced alternative benefit design. As plans make decisions on the 2027 plan offerings and coverage, it is important to understand how these decisions may impact drug utilization and beneficiary access.

Methodology

Avalere Health performed a retrospective, descriptive analysis of county level changes in MA benchmark rates, plan availability, and plan enrollment across the United States and Puerto Rico. All other territories were excluded from this analysis. MA plans examined by this analysis include MA-only plans, Medicare Advantage Prescription Drug plans, and special needs plans. This analysis excludes Prescription Drug Plans, Cost plans, Programs of All-Inclusive Care for the Elderly, Medical Savings Account plans, and Employer Group Waiver Plans.

The county-level benchmark change was calculated as the percentage difference between the 0% bonus benchmark rate in 2027 and the 0% bonus benchmark rate in 2026. County-level benchmark rates were sourced from the MA Ratebook released by CMS for plan years 2026 and 2027. Specifically, the 0% bonus rate was used for each year to ensure comparability across counties regardless of plan-level star ratings.

The number of MA plans available in each county was derived from the CMS Landscape files for 2025 and 2026. The change in plan count was calculated as the difference in the total number of plans offered in a given county in 2026 vs. 2025 to reflect net plan entry and exit activity.

Total MA enrollment per county was summed across all included plan types using the February Monthly Plan Enrollment by County files released CMS for 2025 and 2026. The change in enrollment between 2026 and 2025 was calculated as the change in total enrollees in included MA plan types using the February enrollment by county files released by CMS.

Services

produces measurable results. Let's work together.