Early Learnings from China’s New Commercial Health Insurance Innovative Drug Catalogue

Summary

The recently launched CHI Catalogue signals payer endorsement of high-cost breakthrough therapies supported by strong clinical evidence, real-world data, and guideline endorsement.Introduction

China’s first Commercial Health Insurance (CHI) Innovative Drug Catalogue (商保创新药目录) emerges at a time when national health policy is increasingly focused on strengthening access pathways for innovative therapies. In China’s 15th Five-Year Plan (2026–2030), policymakers introduced ambition to improve reimbursement access for innovative drugs and medical devices. The plan explicitly calls for establishing mechanisms through which medical insurance can support innovative medicines including perfecting the innovative drug catalogue and encouraging commercial health insurance to expand coverage for innovative therapies.

For many years, limited reimbursement access has been a central concern raised by multinational pharmaceutical companies operating in China, particularly for high-cost breakthrough therapies whose prices exceed the affordability constraints of the Basic Medical Insurance (BMI) system. By recognizing this challenge at the highest level of national policy planning, the draft Five-Year Plan signals a structural policy response: expanding the role of commercial insurance and alternative payment pathways alongside the traditional National Reimbursement Drug List (NRDL) reimbursement route.

In July 2025, China’s National Healthcare Security Administration (NHSA) launched applications for the new Commercial Health Insurance Innovative Drug Catalogue in parallel with the annual NDRL cycle. The CHI Catalogue functions as an NHSA-endorsed reference list, signalling to commercial health insurers which high-value innovative therapies may be appropriate for coverage while helping maintain financial sustainability within China’s BMI system. It was introduced to address a reimbursement gap driven by the availability of highly innovative therapies and the affordability constraints of China’s BMI system.

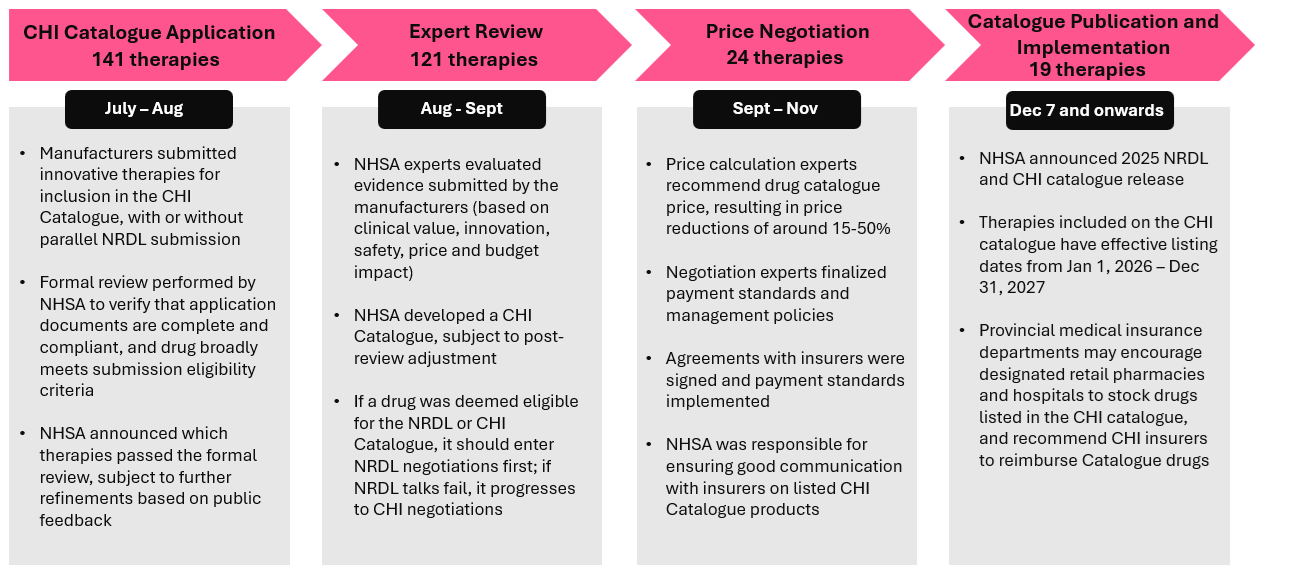

CHI Catalogue: Drug Application to Catalogue Implementation Timeline

Following multi-stage review and negotiations that lasted through November, the CHI Catalogue was published in December 2025. Figure 1 illustrates the end-to-end CHI Catalogue selection funnel, highlighting progressive shortlisting from application to expert review, price discussion, and then final catalogue inclusion.

Figure 1. CHI Catalogue Application Process and Outcome

Under the NRDL framework, manufacturers applying their therapies for Category B (innovative, branded, or higher-cost medications) undergo price negotiations with NHSA. During NRDL negotiations, manufacturers typically have two opportunities to submit price bids. After the first bid, NHSA negotiation experts indicate whether the offer falls within 115% of the confidential envelope price. If both the first and second bids exceed this threshold, the negotiation fails. According to industry experts, implicit cost thresholds (i.e., RMB 500,000 pre-negotiation, RMB 300,000 post-negotiation) may exist alongside the envelope price ratio. As a result, some high-cost therapies with strong clinical value may have struggled to reach the payer’s acceptable price range and may instead be considered for inclusion in the CHI Catalogue.

Of the 121 therapies that passed preliminary review, 42 (34.7%) pursued CHI-only submissions (predominantly in oncology and rare diseases), while the remainder submitted in parallel to both the NRDL and CHI. The high proportion of dual submissions suggests that manufacturers may have viewed CHI as complementary to NRDL rather than as a fully standalone access route. This submission pattern may reflect continued reliance on NRDL as the primary reimbursement pathway under China’s BMI system. At the same time, given that the CHI Catalogue was introduced for the first time, manufacturers may have opted to pursue both pathways concurrently due to uncertainty around negotiation outcomes.

However, the final inclusion of only 19 therapies (13.5% success rate), together with the exceptional clinical profiles of listed drugs, indicates that the inaugural CHI Catalogue applied stringent evidentiary criteria.

In the following sections, we examine the characteristics of listed therapies and the resulting access implications for manufacturers.

Key Characteristics of Therapies Listed on the CHI Catalogue

Therapies included in the inaugural CHI Catalogue exhibit several common clinical and payer-relevant characteristics, including transformational or first-in-class innovation, indications with high unmet need, strong clinical efficacy with manageable safety profiles, endorsement across local and/or international clinical guidelines, and controllable payout risk for commercial insurers (Figure 2).

Transformational / First-in-class Innovation: A substantial proportion of therapies included in the CHI Catalogue are highly innovative, with 8 of 19 (42.1%) classified as Class 1 innovative drugs. This suggests the catalogue may function as an early access signal for breakthrough therapies not previously marketed in China or globally. The catalogue also includes several first-in-class therapies with significant innovation value; for example, ipilimumab – the world’s first CTLA-4 inhibitor – was awarded the Prix Galien (“Discovery of the Decade”).

Indications with High Unmet Medical Need: Many therapies in the CHI Catalogue target rare, serious, or life-threatening conditions. Notably, six of the 19 therapies are also listed in China’s Rare Disease Drug Catalogue, accounting for approximately one-third of the total. These diseases are often associated with poor survival outcomes, reduced quality of life, and/or limited treatment options under current standards of care.

Several therapies also address areas where existing treatments are insufficient or address symptoms instead of the underlying pathology of the disease. For example, disease-modifying therapies donanemab and lecanemab target underlying amyloid pathology in Alzheimer’s rather than symptoms alone. These indications typically involve patients with substantial disease burden, underscoring the need for timely access to innovative treatments. Prioritizing such therapies aligns with broader policy efforts to improve access for patients with severe and underserved conditions.

Exceptional Clinical Efficacy and Safety: Therapies included in the CHI Catalogue demonstrate clinically meaningful, rather than marginal, improvements in outcomes. These benefits are typically shown on payer-relevant endpoints such as overall survival (OS), progression-free survival (PFS), and objective response rate (ORR), often compared against established standards of care or supported by robust clinical and real-world evidence. At the same time, these therapies are associated with favourable safety profiles, with minimal to no grade ≥3 adverse events in some cases. For example, zanidatamab-hrii showed no grade ≥4 adverse events, a threefold reduction in grade ≥3 adverse events, and substantially improved efficacy versus comparator (ORR ~10× higher; median OS ~3× longer). Similarly, equecabtagene autoleucel (Equec-cel) achieved a 98.9% overall response rate and 88.4% complete remission in CAR-T–naïve patients.

These outcomes suggest that inclusion in the CHI Catalogue favours therapies supported by strong clinical evidence demonstrating meaningful, rather than incremental, therapeutic benefit.

Clinical Endorsement Across Multiple Guidelines / Expert Consensus: Many therapies included in the CHI Catalogue are recommended in established local and/or international clinical guidelines. These recommendations often reflect broad expert consensus on their role in standard of care. In many cases, therapies receive high-level (e.g., Grade 1/1A) recommendations, indicating strong confidence that clinical benefits outweigh risks. For example, lecanemab holds Grade 1A recommendations in the 2025 CAAD Alzheimer’s guidelines and is supported by expert consensus from the Chinese Medical Association (CMA).

This alignment with clinical guidelines suggests that inclusion in the CHI Catalogue prioritizes therapies that are already recognized as clinically validated and practice-changing.

Predictable Insurer Payouts: Many CHI-listed therapies target small, well-defined patient populations, limiting overall budget impact and enabling insurers to better forecast utilisation. Treatment is often fixed or time-limited (e.g., capped cycles over a defined period), further supporting predictability of total costs. In addition, manageable safety profiles reduce the risk of high-cost adverse events and downstream expenditure.

While the CHI Catalogue is not legally binding for insurers, these features result in manageable and predictable payouts, supporting sustainable risk pooling and encouraging voluntary adoption by commercial insurers. For example, ipilimumab has a capped treatment duration (four cycles over two years) in hepatocellular carcinoma and colorectal cancer, with average annual costs of RMB 129,600 and RMB 43,000, respectively.

Taken together, these characteristics position CHI-listed therapies for early clinician adoption and facilitate their inclusion in commercial insurance coverage, helping expand patient access to high-value innovative treatments.

Implementation Progress of the CHI Catalogue

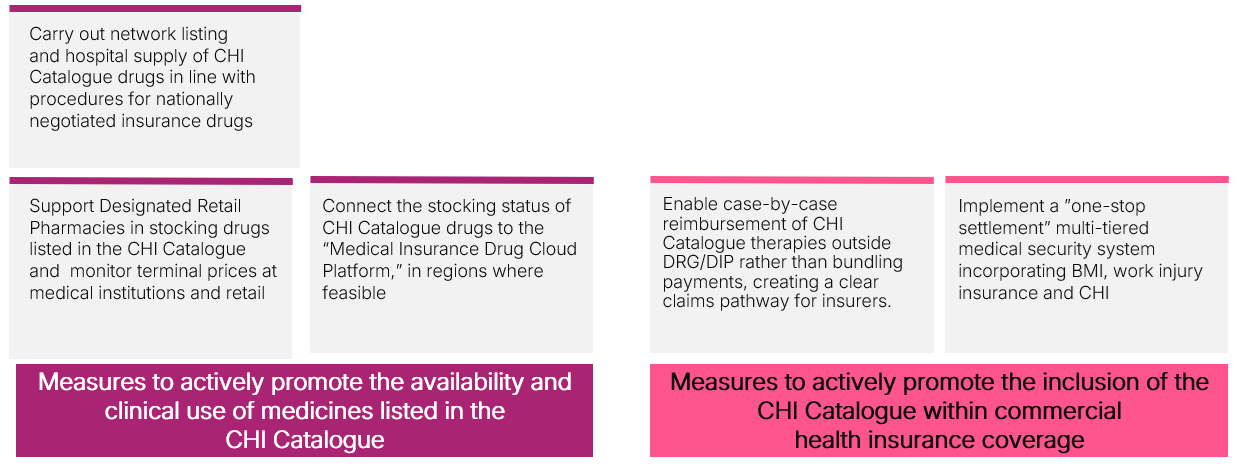

In December 2025, together with the publication of the CHI Catalogue, the NHSA introduced implementation measures to actively promote the availability and clinical use of medicines listed in the CHI Catalogue, as well as the inclusion of the CHI Catalogue within commercial health insurance coverage (Figure 3).

Figure 2. CHI Catalogue Implementation Measures Introduced by NHSA for Provincial Authorities

DIP: Diagnosis Intervention Packet; DRG: Diagnosis Related Group

As of January 2026, the 19 drugs listed in the CHI Catalogue had been made available across 965 designated medical institutions nationwide, including 449 healthcare institutions and 516 designated retail pharmacies. Health Security Administrators in economically developed regions such as Shanghai have issued notifications outlining more detailed implementation policies, while Shenzhen announced in early December that all therapies listed in the CHI Catalogue will be covered under the city’s supplementary commercial insurance scheme (Huiminbao).

However, some private health insurers have expressed reservations regarding pricing and regulatory compliance when designing new insurance products incorporating CHI-listed therapies. Although the NHSA has indicated that it will encourage and support commercial insurers to include these innovative medicines in their products, a clear national roadmap for implementation has yet to emerge. If effectively implemented, these measures could help reduce administrative bottlenecks, improve transparency around drug availability, and facilitate broader distribution of CHI Catalogue therapies across both hospital and retail pharmacy settings.

Early Access Implications of the CHI Catalogue

With ongoing implementation measures, alignment with established clinical guidelines, and manageable insurer payout risk, the CHI Catalogue has the potential to facilitate broader commercial insurance coverage of high-value innovative therapies.

Current evidence suggests that the CHI Catalogue may initially consolidate existing commercial coverage rather than immediately expanding access to treatments. Several listed therapies had already been reimbursed by commercial insurers nationwide prior to catalogue inclusion. For example, the CAR-T therapy axicabtagene ciloleucel was covered by over 80 CHI policies and more than 110 urban Huiminbao programs, while relma-cel was included in over 70 CHI policies nationwide before CHI Catalogue implementation.

In addition, price reductions under CHI negotiations are expected to be more moderate than under NRDL negotiations, with experts estimating reductions of approximately 20–40% compared with 50–70% typically observed for NRDL-listed therapies. Rather than relying solely on price reductions, CHI-listed therapies may combine other payment mechanisms, such as patient assistance programs, to help improve patient affordability.

That said, the first edition of the CHI Catalogue may still improve the geographic consistency of coverage for innovative therapies across China. For instance, ipilimumab was previously listed in 17 Huiminbao programs with <10 annual malignant pleural mesothelioma claims (<RMB 300,000 total payout), but a recent NHSA review (11 January) found it is now stocked in >30 provinces. This suggests that the Catalogue may help standardize the availability of certain innovative therapies across regions, even where earlier commercial coverage existed.

Monitoring provincial implementation, insurer benefit design, actual claims uptake, and patient out-of-pocket burden will be necessary to determine whether Catalogue inclusion translates into meaningful expansion of access beyond policy consolidation.

To find out how we can support you in access strategy for products and portfolios in China, contact us.

Services

produces measurable results. Let's work together.